Equity is dead weight until you move it. A forensic look at leveraging real estate to solve the liquidity gap.

A profitable business should not be denied financing.

Yet I watch it happen every week.

Owners generating $2 million, $5 million, even $12 million in annual revenue walk into a bank confident — and walk out confused. Deposits are strong. Contracts are signed. Growth is visible. But the tax return shows lean net income because the owner reinvested aggressively, depreciated equipment, or optimized for taxes.

The bank doesn’t underwrite momentum. It underwrites paperwork.

That disconnect is costing serious business owners real estate opportunities, equity growth, and strategic control.

From where I sit as an asset-based lending expert, this isn’t a credit problem. It’s a box problem. Traditional underwriting was designed for salaried predictability, not entrepreneurial volatility.

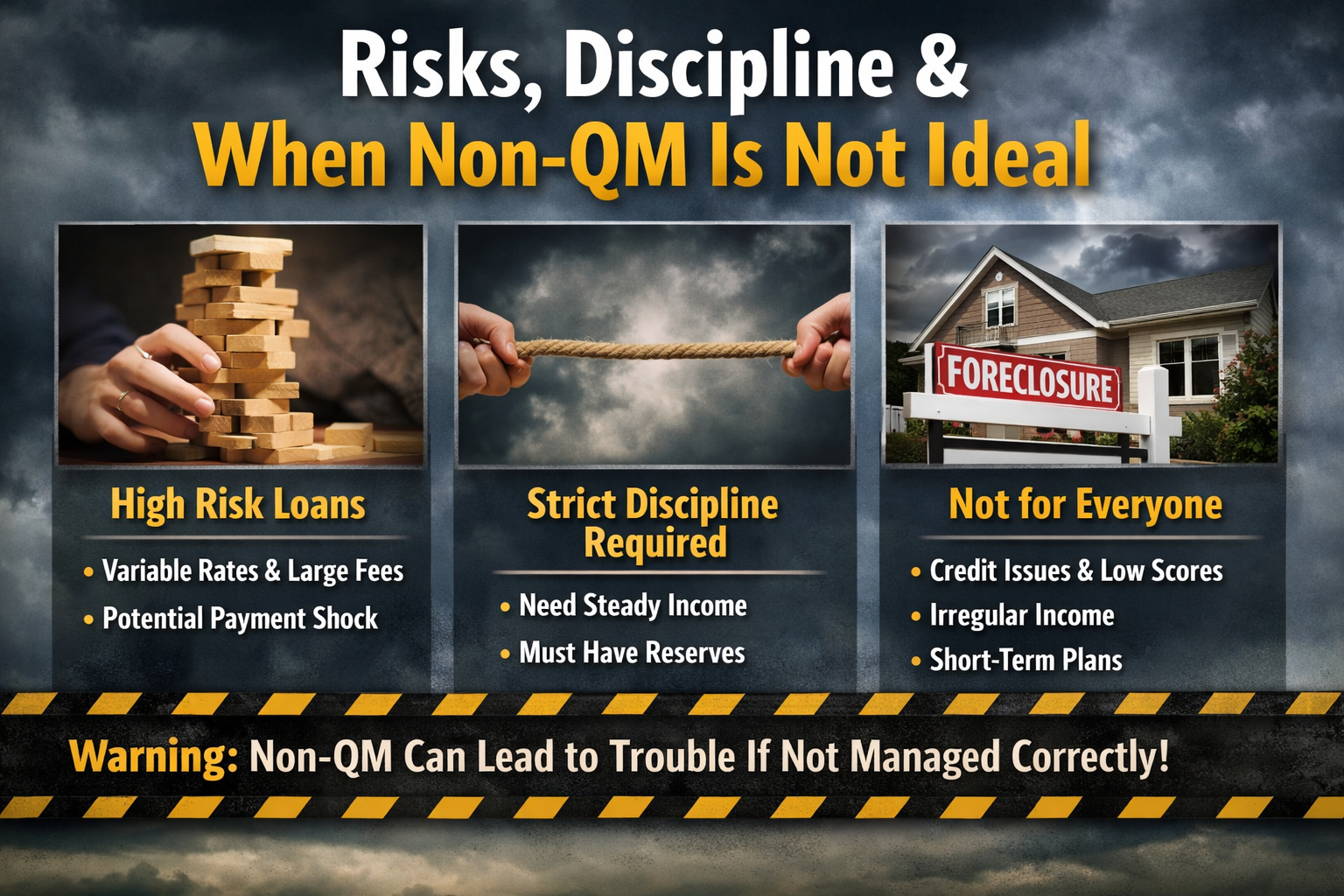

Here’s the shift: Non-QM real estate lending is not “alternative.” It’s structured flexibility that evaluates how your business actually performs.

In 2026, understanding that difference may determine who controls their property — and who keeps waiting for approval.

If you’re building a business between $500K and $20M in revenue, this is capital strategy you cannot afford to misunderstand.

CEO Takeaways

• Bank denials often reflect documentation structure — not business weakness.

• Tax efficiency can unintentionally suppress borrowing capacity.

• Real estate control is a strategic asset, not just a financing decision.

• In 2026, underwriting flexibility may separate expanding owners from stalled ones.

Traditional lending is built around consistency. Predictable W-2 income. Stable year-over-year net profit. Clean entity structures.

Growing businesses rarely look that way.

I work with owners who deliberately lower taxable income. They accelerate depreciation. They expense equipment. They reinvest profits into hiring, marketing, or inventory. On paper, net income shrinks. In reality, the business strengthens.

Banks underwrite the paper.

Then there’s entity complexity. Many owners operate multiple LLCs — one for operations, one for real estate, another for equipment. Cash flows between entities for legitimate tax and liability reasons. To an underwriter applying rigid guidelines, that complexity becomes friction.

And in 2026, friction is increasing.

Credit tightening. Overlay adjustments. Heightened documentation scrutiny. Even strong borrowers are facing narrower approval margins as banks protect balance sheets.

The result is predictable:

When documentation doesn’t reflect real performance, financing stalls.

That’s not because the business lacks capacity. It’s because the underwriting model wasn’t built for entrepreneurial growth cycles.

This is precisely where structured flexibility — including Non-QM programs — becomes relevant.

CEO Takeaways

• Tax efficiency can reduce reported income but not real cash flow.

• Reinvestment strengthens businesses — but can weaken traditional loan approvals.

• Multiple entities add protection, yet complicate conventional underwriting.

• As bank overlays tighten in 2026, flexible documentation strategies become critical.

• If paperwork misrepresents performance, you need financing aligned with reality.

When I evaluate Non-QM for an owner, I’m not looking for a workaround. I’m looking for alignment — between how the business actually performs and how the lender evaluates risk.

Here are the programs that matter most in 2026.

Bank statement programs are often the cleanest solution for self-employed owners.

Instead of underwriting off tax returns, the lender reviews 12–24 months of business (or sometimes personal) deposits. The focus shifts from reported net income to actual cash flow behavior. If deposits are consistent and the expense ratio is reasonable, qualification becomes far more realistic.

I’ve used bank statement loans for contractors, medical practices, logistics firms, and professional services businesses that show strong monthly inflows but limited taxable income.

Use case: purchasing or refinancing an owner-occupied building while preserving working capital inside the company.

This program rewards operational strength — not tax optics.

CEO Takeaways

• Deposits often tell a truer story than tax returns.

• Strong cash flow consistency improves approval odds.

• Ideal for owner-occupied property acquisitions.

• Aligns financing with business reality, not accounting strategy.

P&L programs work well when growth has accelerated recently.

Instead of relying solely on filed tax returns, lenders may accept a CPA-prepared profit and loss statement to reflect current performance. This shortens the look-back window and captures momentum that hasn’t yet shown up in prior filings.

For fast-growing companies — especially those expanding revenue quickly — this flexibility can be critical.

Strategic fit: businesses scaling rapidly where the prior tax year understates present earning power.

I view this as momentum underwriting.

CEO Takeaways

• Rapid growth may not be visible in last year’s tax return.

• CPA-prepared P&L can capture current performance.

• Useful for expansion-stage businesses.

• Financing should reflect today’s numbers — not last year’s snapshot.

DSCR (Debt Service Coverage Ratio) loans shift the focus away from the owner entirely.

Here, the property qualifies based on its own rental income. If the property’s cash flow sufficiently covers the proposed mortgage payment, approval becomes possible — regardless of the borrower’s personal income structure.

For business owners acquiring mixed-use buildings, warehouses with rental components, or standalone investment properties, this structure is powerful.

Capital strategy angle: you build real estate equity while preserving liquidity inside your operating company. The property carries itself.

That separation is strategic. It keeps your business capital intact while your real estate grows independently.

CEO Takeaways

• Property cash flow can qualify the loan.

• Owner income becomes secondary.

• Strong fit for investment or mixed-use real estate.

• Enables equity growth without draining business liquidity.

This is one of the most overlooked capital tools available.

A standalone second allows you to access equity without refinancing your existing first mortgage. If you locked in a strong rate two or three years ago, you preserve it. You don’t disturb the first lien.

Instead, you tap a portion of available equity as structured liquidity.

Use case: funding inventory, equipment, expansion, or short-term working capital — without selling ownership or restructuring existing debt.

From a capital efficiency standpoint, this is intelligent layering. You optimize what you already own.

CEO Takeaways

• Access equity without touching your low first-lien rate.

• Avoid unnecessary refinancing risk.

• Generate liquidity without equity dilution.

• Strong tool for expansion capital.

Entrepreneurship does not require a traditional SSN profile.

ITIN programs expand access to real estate financing for borrowers without standard Social Security documentation. These programs evaluate credit behavior, income documentation, and asset strength within structured guidelines.

I’ve seen immigrant entrepreneurs build exceptional businesses yet struggle with conventional mortgage qualification. This structure acknowledges real economic contribution.

It’s inclusion through underwriting design.

CEO Takeaways

• Real estate financing is possible without traditional SSN documentation.

• Expands access for entrepreneurial business owners.

• Structured flexibility — not lowered standards.

• Ownership control remains the objective.

Each of these programs serves a different strategic purpose. The key is not choosing the “easiest” option. It’s choosing the structure that aligns with how your business truly performs and where you intend to grow.

I want to challenge the narrative right here.

Non-QM is not what you use when you “can’t qualify.”

It’s what you use when you understand capital structure.

Too many business owners treat financing as a pass/fail test administered by a bank. Approval becomes validation. Denial becomes discouragement. That mindset gives the bank too much control over your growth timeline.

From where I sit, Non-QM is a structural choice.

-It protects equity.

-It avoids bringing in outside investors prematurely.

-It allows you to acquire or refinance real estate without diluting ownership in your operating company.

If your business generates strong deposits but optimizes taxable income, your financing structure should reflect that reality. If your growth trajectory doesn’t fit a conventional underwriting box, the box shouldn’t dictate your strategy.

Smart owners use tools intentionally.

Reactive owners wait for approval.

The difference is control.

In 2026, the businesses that expand intelligently will be the ones that understand financing as architecture — not permission. Non-QM programs are simply one more lever in a disciplined capital plan.

CEO Takeaways

• Financing is a capital structure decision — not a validation test.

• Non-QM can preserve equity and prevent unnecessary dilution.

• Control over property equals control over long-term leverage.

• Underwriting should align with real performance, not rigid templates.

• Strategic owners choose tools; reactive owners wait for approval.

Let me make this practical.

A contractor generating roughly $4 million in annual revenue wanted to purchase the warehouse he had been leasing for years. Deposits were strong. Backlog was healthy. But taxable income was compressed due to equipment write-offs and aggressive reinvestment.

The bank focused on net income. The numbers didn’t fit.

We structured a bank statement loan instead. Underwriting evaluated 24 months of consistent business deposits, not paper-adjusted profit. He closed on the warehouse, fixed his occupancy cost, and began building equity in an appreciating asset.

The capital outcome:

He converted rent into ownership without draining operating liquidity.

A retailer doing $2.5 million annually had locked in an attractive first mortgage rate two years prior. Business was expanding, and inventory needs were increasing ahead of peak season. Refinancing the entire property would have meant losing that favorable rate.

Instead, we layered a standalone second mortgage. The first lien remained untouched. The retailer accessed structured liquidity tied to existing equity and used it to expand inventory and improve vendor terms.

The capital outcome:

Growth was funded without selling equity or disturbing low-cost debt.

CEO Takeaways

• Strong deposits can unlock ownership even when taxable income is lean.

• Real estate equity can fund growth without refinancing everything.

• Preserving low-rate debt is often smarter than restructuring it.

• Capital structure decisions should enhance flexibility — not create friction.

Non-QM is a tool — not a shortcut.

Rates may be higher than conventional bank products. That’s the tradeoff for underwriting flexibility. If you qualify cleanly for a traditional QM mortgage at the lowest possible rate, you should absolutely compare the economics carefully.

Loan-to-value limits can also be tighter. Lenders want meaningful borrower equity in the deal. Strong deposits and documented cash flow consistency matter. If revenue is volatile or deposits swing wildly month to month, approval becomes more difficult.

And this is important: Non-QM is not rescue capital for distressed borrowers. It works best for fundamentally healthy businesses that simply don’t fit conventional underwriting boxes.

From my perspective, discipline is everything. The structure must make strategic sense. The cost of capital must align with the return on the property or the growth it supports.

Flexibility without discipline becomes expensive.

Used correctly, Non-QM enhances capital structure. Used carelessly, it compresses margins.

CEO Takeaways

• Compare cost of capital carefully — flexibility has a price.

• Expect realistic LTV limits and equity requirements.

• Consistent deposits strengthen approval probability.

• Non-QM supports healthy businesses — not distressed situations.

• Capital tools require discipline, not urgency.

I’m watching two trends move in opposite directions.

Banks are tightening. Documentation standards are hardening. Credit committees are becoming more conservative as balance sheets are protected and risk models recalibrated.

At the same time, alternative underwriting is expanding — becoming more structured, more institutional, and more aligned with how real businesses actually operate.

That divergence creates opportunity.

The owners who win in 2026 won’t be the ones waiting for approval. They’ll be the ones who understand how their capital is structured — and how real estate fits into that architecture.

Control matters.

Equity matters.

Liquidity matters.

Real estate is not just an asset. It is leverage, stability, and long-term strategic positioning.

Review your real estate position.

Understand your options.

Structure capital intentionally.

Here's a question that separates $10 million businesses from $2 million ones: When was the last time you changed operations because of something you saw coming, not something that already hit you?

Most operators excel at reacting. Problem shows up, they solve it. That keeps you alive. It doesn't make you grow.

I just watched a business owner lose a $2.3 million contract to a competitor who made one strategic change eighteen months ago. Same industry. Similar capabilities. One saw the shift early. The other is still wondering what happened.

After over twenty years financing businesses across every sector, I've learned something counterintuitive: the best operators aren't visionaries. They don't predict the future.

They're just disciplined about watching what's already changing and moving before it becomes urgent.

The gap between early movers and late reactors isn't closing. It's accelerating. And 2026 is the year that gap becomes impossible to ignore.

These trends cut across technology, workforce dynamics, capital access, and operational strategy. Will every single one apply to your business?

No. But I guarantee at least three are already impacting your bottom line whether you've noticed or not.

Miss the ones relevant to your industry, and you're looking at six-figure consequences—lost contracts, talent walking out the door, opportunities your competitors grab while you're still figuring out what changed.

Experienced operators aren't trying to master all ten. They're identifying which two or three matter most for their specific situation and moving decisively on those.

A manufacturer I work with just lost a $400K contract. The competitor responded to the RFP in four minutes with a detailed quote. My client took two days because his estimator was on vacation.

Four minutes versus two days. The competitor used AI—automated quoting system that pulled specs, cross-referenced inventory, generated a proposal. Done.

That's where we are. AI isn't some future consideration. It already decided who won that contract.

Your customers expect instant responses now. Order tracking without phone calls. Systems that remember their preferences. If your competitor delivers and you're manually doing everything? You look slow.

Back office tells the same story. Scheduling, bookkeeping, inventory updates—businesses hitting $10 million aren't drowning in admin staff. They automated repetitive tasks years ago.

The numbers? Companies using AI for customer service cut response times 30-40%. Those automating admin work free up ten hours weekly per employee.

Ten hours. What could your best people do with an extra ten hours?

Stop waiting for perfect. Your competitors aren't.

Pick one thing this quarter—automate quoting, customer service, or bookkeeping

AI separates winners from losers today, not someday

Customers expect it; you're losing deals without it

The hiring crisis didn't end. It just stopped being about money.

A logistics company lost their best operations manager last month. Competitor offered $8K more annually. Sounds straightforward?

Wrong. The real reason? Three remote days weekly versus five days in-office.

$8K didn't matter. Flexibility did.

Workers stopped chasing pay bumps. They want flexibility, growth, and work that doesn't feel pointless. Skills-based hiring overtook degrees. A developer with a portfolio beats a CS degree with no projects.

Turnover costs 1.5-2x annual salary. Recruiting, onboarding, lost productivity. Businesses stuck in old playbooks pay repeatedly.

Flexibility costs nothing. Replacing good people costs everything.

Workplace flexibility is cheaper than turnover—offer it

Invest in development to keep people, not just attract them

Proven skills beat credentials—rethink requirements

Banks stopped lending to the middle. If you're doing $500K to $20M in revenue, you know this.

They want perfect financials. Pristine ratios. Collateral fitting exact templates. One tough quarter? Denied. Tax write-offs lowered reported income? You don't fit the box.

Alternative lenders stepped in. Asset-based financing, revenue-based lending, equipment lines. They evaluate what you own and how cash flows, not tax returns.

A distribution company got turned down by two banks. Needed $750K for inventory. Third bank also said no. Asset-based lender approved them in eleven days using paid-off forklifts as collateral.

Same business. Different lender, different result.

The operator knowing only traditional banking? Limited options. The one knowing alternatives? Moves when opportunity shows up.

Learn alternatives before you desperately need them

Structure and speed often matter more than rate

Multiple capital sources give you leverage

Facebook ads used to work. Spend $50, get three customers, make $400.

Not anymore.

Digital ad costs jumped 30-40% while organic reach collapsed. Posts that hit 10,000 people now reach 300. Paid acquisition? You're spending $200 to get a customer worth $150.

That's not growth. That's bleeding money.

What works now? Community. Retention. Referrals. Lifetime value.

A Texas service company cut acquisition spending 40% and reinvested in customer experience. Faster responses, better follow-up, loyalty rewards.

Six months later: referral rates doubled, customer lifetime value jumped 60%. Same revenue, better margins, sustainable.

Businesses dumping money into broad campaigns are getting crushed. The ones building communities and optimizing retention? Winning quietly.

Retention always cost less. We forgot when ads were cheap.

Key Takeaways:

If CAC rises faster than LTV, your model is broken

Retention beats acquisition—invest accordingly

Build referral engines and community, not ad campaigns

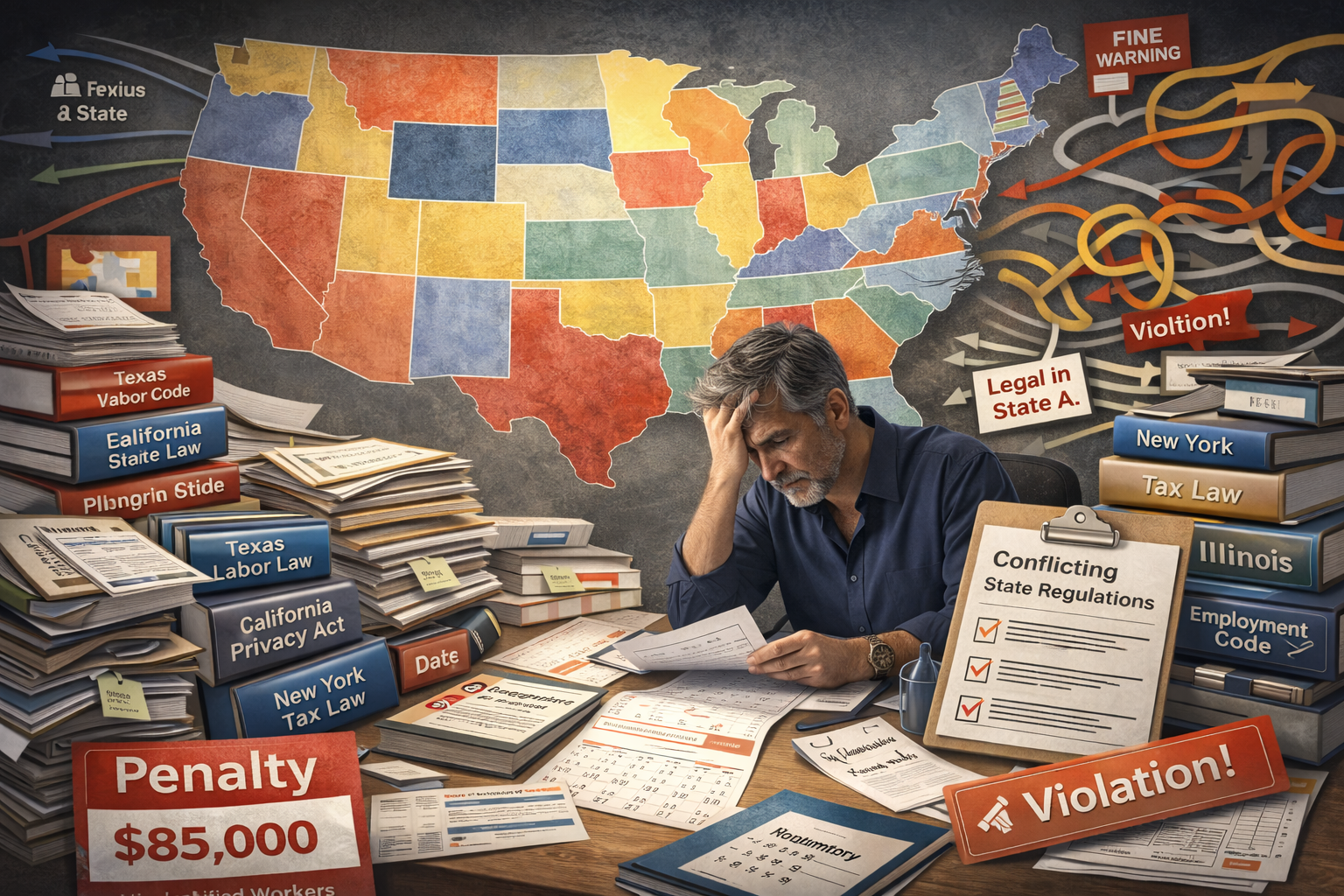

State regulations diverged faster than anyone expected. Labor laws, privacy rules, tax codes—what's legal in Texas isn't in California or New York.

Multi-state operators face compliance nightmares that didn't exist five years ago.

Penalties got aggressive. The "we didn't know" defense? Doesn't work anymore. A Colorado contractor expanded into California without checking local labor laws. Got hit with $85K in fines for misclassified workers.

Growing into new states now requires legal planning upfront, not reactive fixes after violations.

Budget for compliance if you're multi-state. Don't assume what works in one place transfers automatically. Ignorance became expensive in 2026.

Key Takeaways:

Multi-state operations need dedicated compliance resources—budget for it

State regulations diverged dramatically—don't assume portability

Proactive compliance costs less than reactive penalties

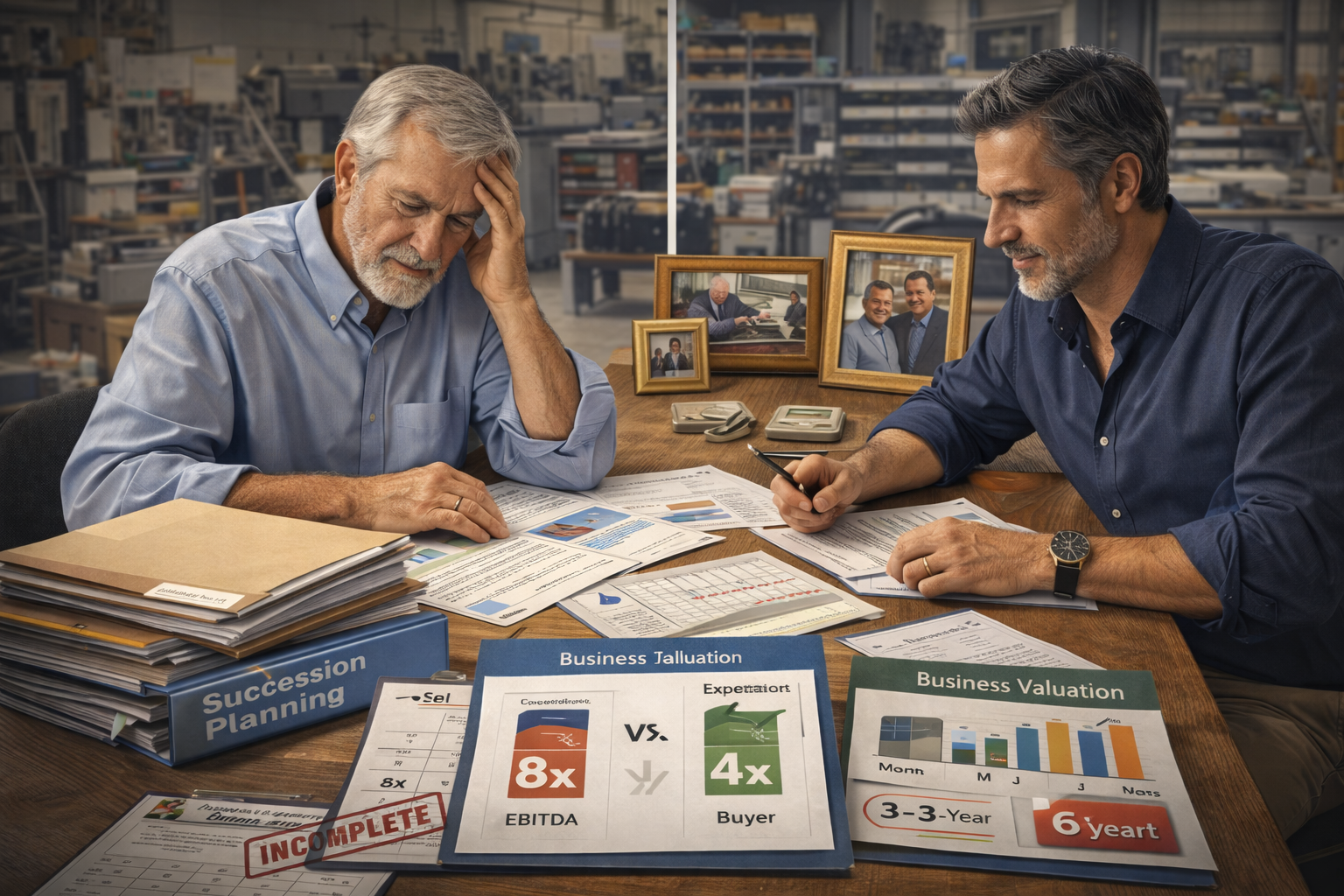

Seventy percent of family businesses will change hands within the next decade. Boomers are exiting. Millennials and Gen Z are taking over.

Buyer-seller expectations? Completely misaligned.

Exit planning takes 3-5 years, not six months. Sellers remember deals structured one way. Buyers expect different terms today.

A manufacturing business owner I know assumed his son would just "take over when ready." No valuation, no transition plan, no operating agreement. Son wanted equity immediately, not after Dad retired. Deal nearly collapsed.

Succession isn't paperwork. It's strategic, emotional, and financially complex.

The generation taking over brings different operating assumptions. What worked for 30 years won't survive the transition without deliberate planning.

Key Takeaways:

If you're 55+, start exit planning now—even if you're not selling soon

Buyers and sellers are misaligned on structure—education matters

Succession planning is strategic, not administrative

Single-source suppliers are now high risk. Post-pandemic lessons stuck.

Inventory strategies shifted from "just in time" to "just in case." Nearshoring and supplier diversification became standard.

Small businesses can't absorb shocks like Fortune 500 companies. That makes resilience critical.

Build relationships with 2-3 suppliers, not one. Understand your critical dependencies. A small buffer inventory costs money but saves more when disruptions hit.

A furniture maker relied on one Chinese supplier. Container delays killed Q4 sales. Next year? Two backup suppliers, one domestic. Costs rose 8%. Lost sales dropped to zero.

Supply chain disruptions aren't over. They're permanent. Redundancy costs less than lost sales.

Key Takeaways:

Supply chain disruptions are permanent—plan accordingly

Supplier redundancy costs money but saves more during disruptions

Know your critical dependencies cold

When products commoditize, service separates winners from losers. Most industries face product parity now.

Speed, responsiveness, personalization—these matter more than ever.

The "Amazon effect" raised expectations everywhere. People expect seamless experiences whether buying shoes or hiring contractors.

Small businesses have an advantage here. You can out-service big competitors. Personal touch scales better than corporate bureaucracy. Loyalty built on experience outlasts price competition.

A Michigan HVAC company invested in same-day service guarantees and post-appointment follow-ups. Referral rates jumped 45%. Customer lifetime value increased 35%.

Service became their moat.

Key Takeaways:

Compete on experience when you can't compete on price

Responsiveness beats perfection in most customer interactions

Small businesses win on relationship depth—use that advantage

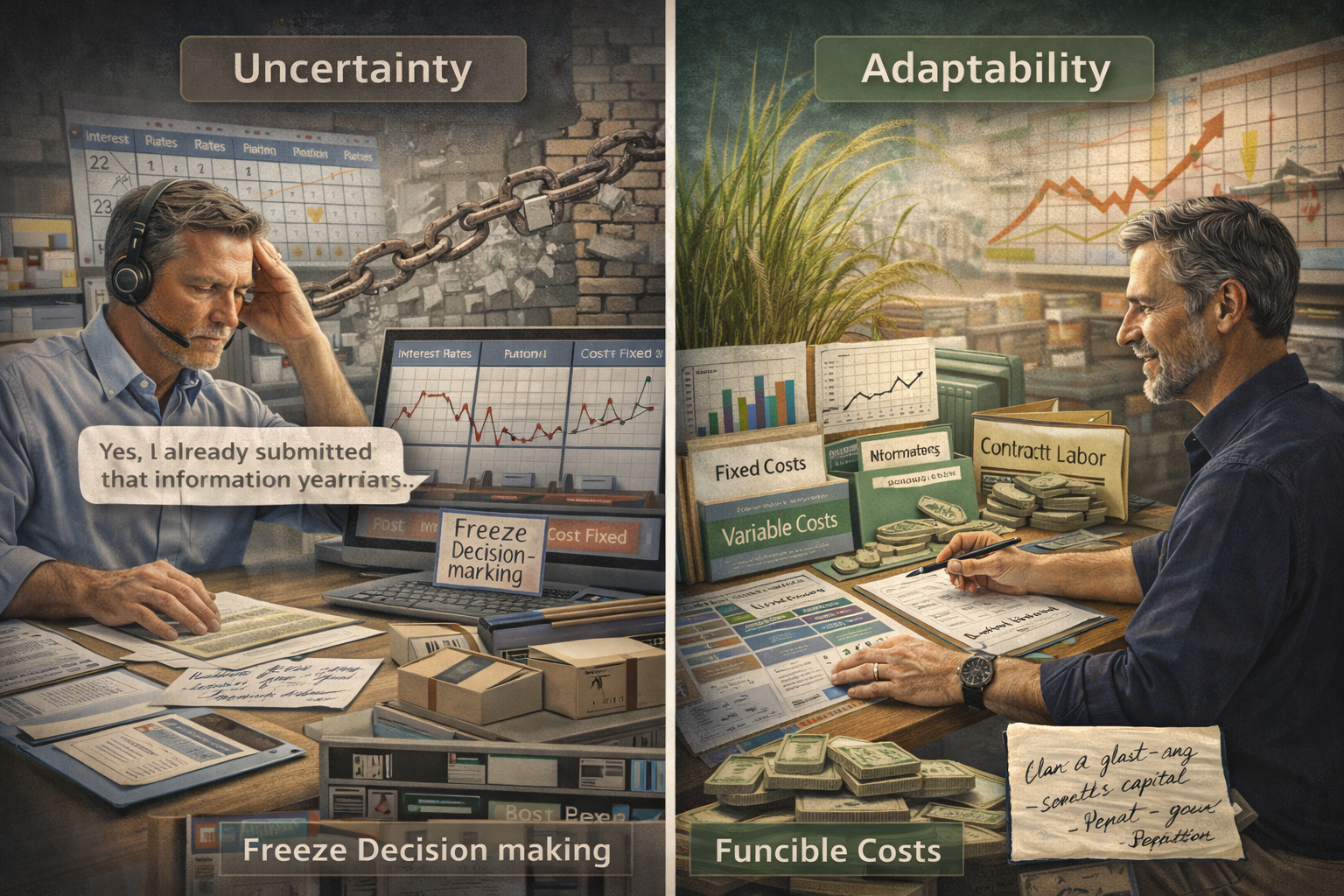

Interest rates, inflation, geopolitical risk—none of it is going away.

Operators who "wait and see" get beat by those who adapt quickly.

Building resilient operations means maintaining 3-6 months cash reserves. Keep cost structures flexible where possible. Use scenario planning instead of rigid annual budgets.

A Pennsylvania manufacturer built variable cost structures using contract labor during peak seasons. When demand softened, costs adjusted automatically. Competitors with fixed overhead struggled.

Don't freeze in uncertainty. Your competitors won't. Adaptability matters more than prediction.

Key Takeaways:

Build 3-6 months operating cash reserves minimum

Flexible cost structures beat fixed overhead in volatile markets

Scenario planning beats rigid annual budgets

Legacy systems became liabilities. Outdated software creates operational drag. Integration failures waste time. Cybersecurity risks multiply with aging infrastructure.

Cloud-based tools aren't optional anymore. API integrations reduce manual work. Security can't be an afterthought.

A distribution company ran operations on a 15-year-old system. Data entry took hours daily. Customer orders got lost. They finally migrated to cloud-based software.

Manual work dropped 60%. Order accuracy jumped to 99%. Customer complaints disappeared.

Audit your tech stack. What's holding you back? Invest in systems that integrate, not isolated tools.

Cybersecurity breaches cost more than prevention.

Key Takeaways:

Audit your tech stack—identify what's creating drag

Invest in integrated systems, not isolated tools

Cybersecurity breaches cost more than prevention

Twenty years financing businesses taught me one thing: winners don't wait for certainty.

They see change coming and move while everyone else is still debating whether it's real.

These ten trends aren't coming—they're here. Your competitors are already adjusting. They're automating customer service. Building referral engines. Diversifying suppliers. Planning exits. Moving capital faster.

You don't need all ten. Pick two that hit your business hardest. Act this month, not next quarter.

The businesses that win 2026 won't be the smartest or best-capitalized. They'll be the ones who recognized what changed and did something about it while others were still reacting to last year's problems.

Which trend matters most to your business? And what's stopping you from addressing it right now?

Most business owners I talk to realize they're sitting on opportunities they didn't know existed. Not because the opportunities weren't there—because nobody showed them what to look for.

If you're running a $500K-$20M revenue business and any of these ten trends hit home, the question isn't whether you should act. It's which one you tackle first.

Corey Rockafeler has spent over twenty years helping operators structure capital around what they already own—equipment, real estate, securities, cash-flowing assets. Most conversations start with a simple question: what's sitting on your balance sheet that could be working harder for your business?

Not a loan application. Not a pitch. Just an honest look at what you control and whether it could fund the move you've been waiting to make.

Contact: corey@ravenbanq.com | 407-255-2542

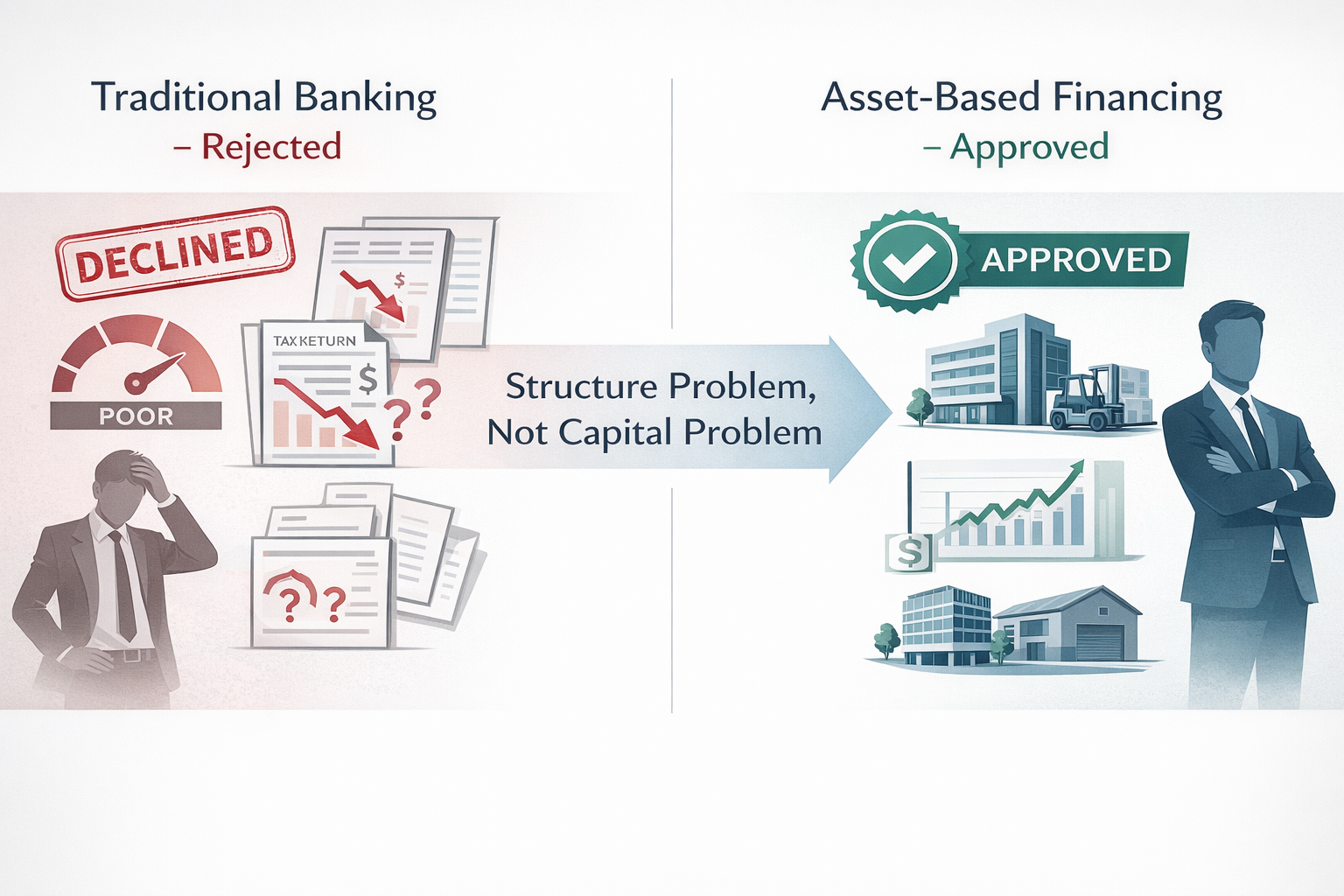

Last Tuesday, a manufacturing CEO called me about a $2M equipment loan denial. His EBITDA looked weak on paper—growth phase, heavy reinvestment; you know the drill. Banks saw the numbers and ran. Here's what they missed: He owned $4.3M in paid-off machinery sitting on his balance sheet. The capital was there. The structure wasn't.

Most businesses don't have a capital problem—they have a structure problem. Banks evaluate you using frameworks built for W-2 employees and Fortune 500 corporations. Strong assets but unconventional structure? You get declined. Tax write-offs make income look low. Denied. Profitable church with congregational giving instead of audited financials? Sorry.

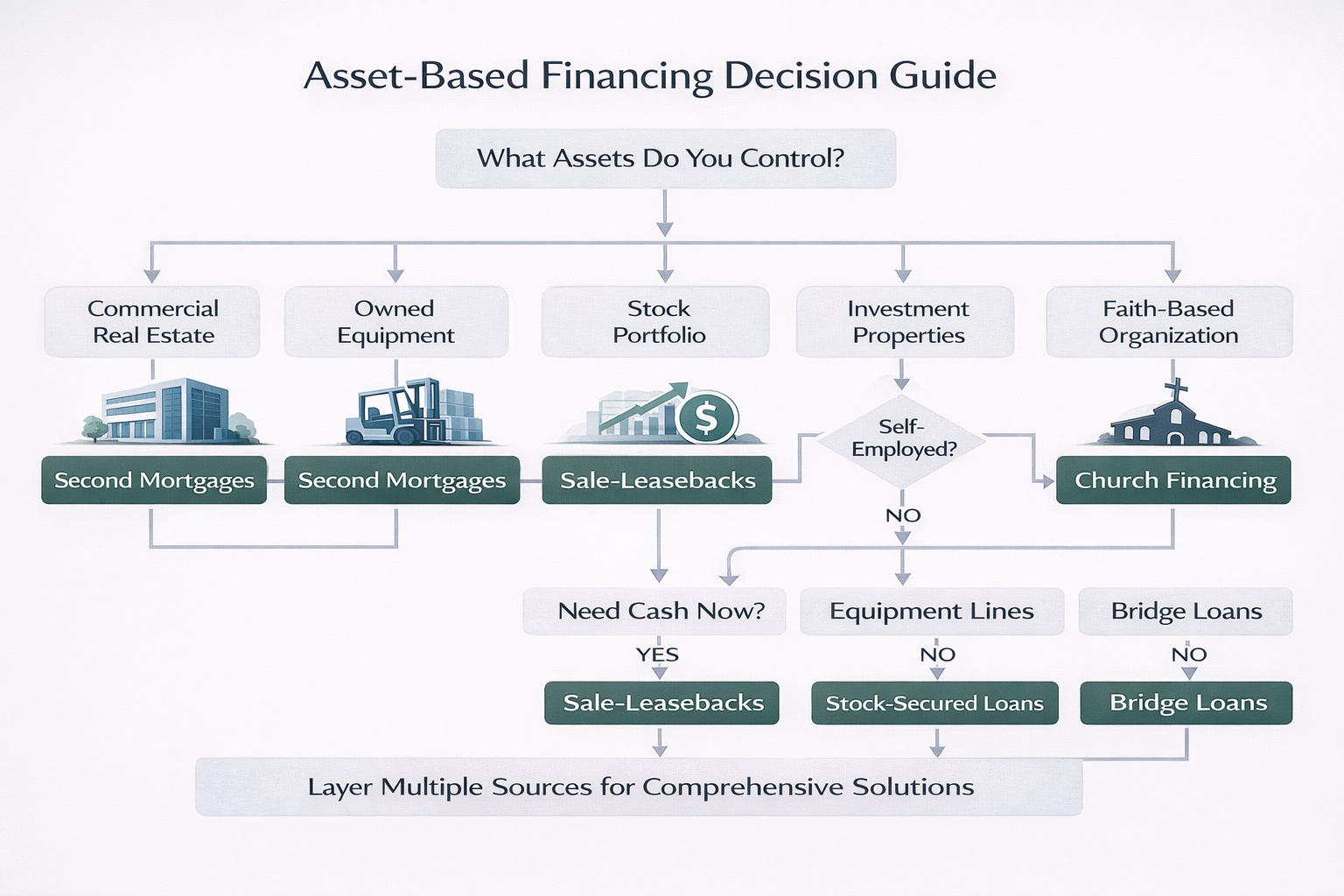

Here's what lenders won't tell you: If you're running $500K to $20M in revenue and hold valuable assets—equipment, real estate, stock portfolios, investment properties—you likely qualify for substantial capital. Just not through conventional channels.

In this article, you'll discover the eight asset-based financing options that work when traditional banks say no.

Asset-based financing is capital secured by what you own, not what your tax returns show or what your credit score says. Lenders evaluate specific collateral—commercial real estate, equipment, securities, cash-flowing properties—and advance funds based on asset value and equity position.

The fundamental difference? Traditional banks assess your personal financials first, then consider collateral as backup security. Asset-based lenders flip this. They start with the asset. Is there equity? Is it liquid? Can we secure our position? Your FICO score, debt-to-income ratio, and tax return complexity become secondary considerations.

It's financing based on what you control, not how you look on paper.

🔑 Key Takeaway: Asset-based financing evaluates collateral value first, personal financials second—making it accessible to businesses that banks typically decline despite having strong balance sheet assets.

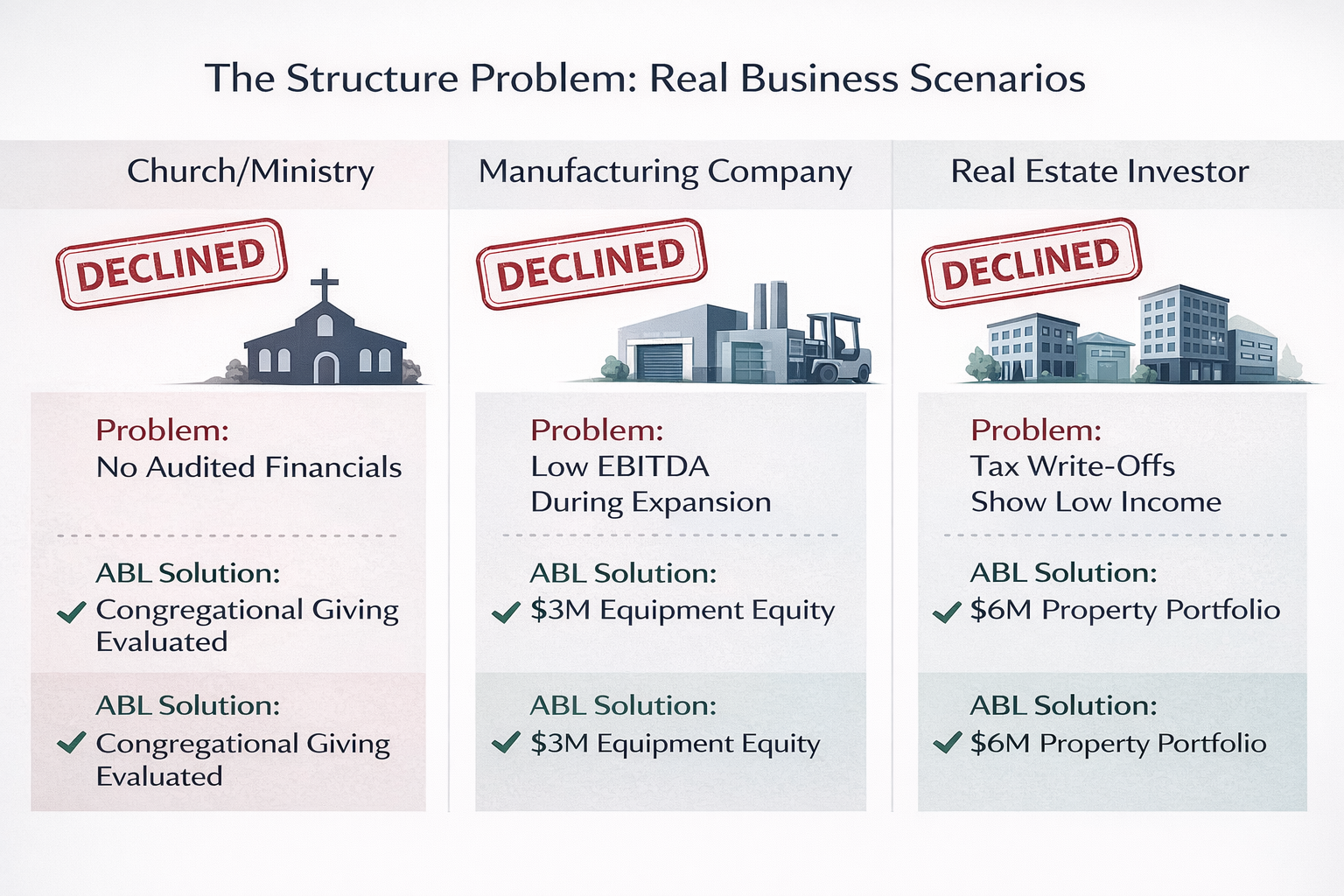

Banks don't reject deals because your assets aren't strong—they reject them because your assets don't fit their policy templates.

I've watched this pattern for 20 years. A church with $800K in annual giving gets declined because there are no audited financials. A distribution company with $3M in paid-off forklifts can't get approved because last year's EBITDA dipped during warehouse expansion. A real estate investor controlling $6M in properties gets denied because aggressive tax write-offs make W-2 income look weak.

The assets are there. The equity is real. The problem is structural.

Asset-based financing solves structure problems, not capital problems. When you don't fit the conventional box but hold valuable collateral, these lenders evaluate deals on economics and equity position—not policy checklists designed for different business models.

Sound familiar?

🔑 Key Takeaway: Traditional bank rejections usually signal a structure mismatch, not weak financials—asset-based lenders evaluate your actual collateral value rather than whether you fit their underwriting template.

OPTION 1: Church Real Estate Financing

Churches face a paradox. Growing congregations need facilities. Banks need audited financials, personal guarantees from board members, and income documentation that doesn't account for how faith-based organizations actually operate. I worked with a ministry last year—$1.2M in annual giving, 400-member congregation, zero debt. Traditional lenders wouldn't touch it.

Look for church lenders who underwrite on underlying financial strength. This type of Church real estate financing evaluates congregational strength, giving history, and ministry trajectory instead of conventional metrics. No audited financials required. No personal guarantees exposing pastors or board members to liability. No minimum FICO thresholds. These programs understand that a church's balance sheet looks nothing like a widget manufacturer's—and that's fine. Loan amounts typically range from $250K to $10M+ depending on property value and congregational capacity. Purchase, refinance, or construction—all structured around how ministries actually function.

OPTION 2: Second Mortgages for Business Owners

Here's what most business owners miss: You can access commercial real estate equity without touching your first mortgage. This matters when your existing rate is 4.5% and current refi rates are 7%+.

Second position loans let you borrow against property equity while preserving your favorable first mortgage. Works on any cash-flowing property—office buildings, retail centers, industrial facilities, mixed-use developments, investment properties. The math: Property worth $2M with a $1M first mortgage at 65% combined loan-to-value means $300K available capital without refinancing.

Available nationwide. No minimum FICO requirement. $100K to $3M loan amounts. Typically funded in three to four weeks. I've closed these for business owners needing acquisition capital, equipment purchases, debt consolidation, or bridging seasonal cash flow gaps. Your building has equity. Use it without blowing up a great first mortgage rate.

OPTION 3: Equipment Secured Term Loans & Lines of Credit

Manufacturing, distribution, construction, transportation—these businesses often have millions in equipment equity sitting idle on balance sheets. A construction company I worked with owned $4M in excavators and dozers outright. Cash flow was tight during a project gap. Banks wanted 750+ FICO and strong EBITDA. We secured $1.8M against the equipment in 19 days.

Equipment-secured financing works two ways. Term loans provide lump-sum capital for specific needs—expansion, acquisitions, major purchases. Revolving lines let you draw funds as needed and pay down as cash flow allows, similar to a credit card but secured by machinery.

Unlike traditional equipment loans requiring pristine financials, these evaluate asset value. Companies use this capital for growth, seasonal inventory, payroll bridging, or working capital during margin compression. Your equipment already exists. Turn it into accessible capital.

OPTION 4: Equipment Sale-Leasebacks

Most overlooked capital source in small business: Sell equipment you own outright, then lease it back under favorable terms. You generate immediate cash. Operations don't skip a beat. You continue using the same machinery under a lease agreement structured around your cash flow.

A metal fabrication shop had $2.8M in paid-off CNC machines. Needed $1.9M for a competitor acquisition. We structured a sale-leaseback—they got the capital, leased the equipment back at competitive rates, closed the acquisition. Twenty-three days start to finish.

This works when you've tied up too much capital in equipment purchases and now need liquidity for opportunities, debt payoff, or operational needs. The equipment becomes a financing tool, not just a production asset. Transactions typically close in 21-30 days.

OPTION 5: Equipment Financing & Leasing

New equipment costs real money. Tying up cash reserves or credit lines to buy it outright creates opportunity cost—that capital could fund marketing, hiring, or inventory instead.

Equipment financing provides 100% financing on new or used assets—machinery, vehicles, technology, specialized equipment. Unlike bank loans demanding 20% down and perfect credit, these programs evaluate the equipment itself as primary collateral. A landscaping company needs three new mowers at $180K total. Banks want $36K down. Equipment financing? Zero down, structured payments matching seasonal revenue.

Options include capital leases (rent-to-own), operating leases (true rental with return option), or term loans secured by the equipment. Payments can be monthly, quarterly, or seasonal. Works for construction equipment, medical devices, restaurant buildouts, manufacturing machinery, delivery fleets—anything with resale value.

OPTION 6: Stock-Secured Loans (Securities-Based Lending)

High-net-worth business owners and executives holding substantial publicly traded stock portfolios face a dilemma. Selling shares triggers capital gains taxes. Not accessing the wealth leaves opportunities on the table.

Stock-secured loans let you borrow 50-70% of portfolio value using securities as collateral. No credit check. No personal guarantee. No income verification. A founder I worked with held $8M in company stock post-IPO. Wanted to acquire a competitor for $3.5M. Selling stock meant $800K+ in taxes. We secured a $4M stock loan—he funded the acquisition, kept his equity position, avoided the tax hit.

Particularly valuable for concentrated positions, executives in lockup periods, or investors preserving stock appreciation while accessing capital for business investments, real estate, or other opportunities. Loan amounts typically start $1M and can reach $50M+ for large portfolios.

OPTION 7: Non-QM Loans for Business Owners

Self-employed business owners live this frustration daily. Business is profitable. Cash flow is strong. Tax returns show $60K income because your CPA correctly maximized write-offs. Traditional mortgage lenders see the $60K and deny you.

Non-Qualified Mortgage (Non-QM) loans evaluate income differently. Bank statement programs analyze 12-24 months of business deposits—they see actual cash flow, not tax-optimized income. Profit & loss programs use CPA-prepared financials. DSCR (Debt Service Coverage Ratio) loans qualify purely on rental property cash flow with zero personal income verification.

Foreign nationals access financing with no U.S. credit history required. A real estate investor I worked with—1099 income, six rental properties, wrote off everything legally possible. Tax returns showed $48K. Bank statements showed $280K in deposits. Non-QM lender approved based on actual cash flow, not paper income.

OPTION 8: Investor & Commercial Real Estate Financing

Speed kills deals. Traditional banks take 60-90 days for commercial real estate approval. You're competing against cash buyers closing in two weeks. You lose.

Bridge loans close deals in 14-21 days when timing matters. Portfolio loans finance multiple properties under one structure when individual banks won't handle complex holdings. Alternative commercial lenders evaluate property fundamentals—location, cash flow, tenant strength, exit strategy—rather than requiring perfect personal financials.

Last month, a developer found a $3.2M mixed-use property. Seller needed to close in 18 days for 1031 exchange timing. Traditional banks couldn't move that fast. We structured bridge financing, closed in 16 days. He later refinanced into permanent financing after renovation.

Particularly valuable for acquisitions, value-add repositioning, construction, or any deal where timing creates competitive advantage.

🔑 Key Takeaways:

Churches, equipment-heavy businesses, stock portfolio holders, and self-employed owners each face unique financing barriers that asset-based options specifically address

Multiple programs can be layered—second mortgages for major capital, equipment lines for ongoing flexibility

Speed and structure often matter more than rate when opportunities have tight timelines

The right asset-based financing option depends on three factors: what assets you control, your capital timeline, and your intended use of funds.

Quick assessment. Own commercial real estate with equity? Second mortgages unlock that capital without refinancing. Own equipment outright but need working capital? Sale-leasebacks convert machines to cash. Self-employed with investment properties? Non-QM or DSCR loans ignore tax returns and evaluate actual cash flow. Hold a stock portfolio but need business capital? Stock-secured loans preserve your equity position. Church or ministry? Specialized programs exist that understand congregational economics.

Here's the reality most businesses miss: You can layer multiple sources. A second mortgage funds major expansion. An equipment line provides ongoing operational flexibility. Most of my engagements start with a balance sheet asset review, not a loan application.

We find what you already own, then structure capital around it.

🔑 Key Takeaway: Asset-based financing isn't one-size-fits-all—the optimal structure combines what you own, when you need capital, and what you'll use it for, often layering multiple sources for comprehensive solutio

Ravenbanq operates as an asset-based capital advisor, not a lender or broker. We don't push single products or represent one funding source. We align structure, timing, and asset strategy across multiple capital sources to match your specific situation.

I've closed $250M+ in asset-based transactions over 20 years. Worked under NYC Mayor Bloomberg partnering with Fortune 500 brands. I've seen deals structured brilliantly and watched others collapse from preventable mistakes.

We identify opportunities in your balance sheet that single-lender shops and rate-quote brokers miss entirely.

🔑 Key Takeaway: Independent advisory beats single-lender or broker relationships—we optimize across all eight asset-based options simultaneously, not just the programs one lender offers.

If your business holds underutilized assets—paid-down real estate, owned equipment, stock portfolios, investment properties—an advisory review often uncovers capital you didn't know was accessible.

Most engagements start with a balance sheet asset review, not a loan application. We identify what you own, then structure financing around it.

Schedule a complimentary asset review: [corey@ravenbanq.com or call 407-255-2542]

Corey Rockafeler is CEO and founder of Ravenbanq, an asset-based financing advisory specializing in small business capital optimization.

As an asset-based financing expert with 20+ years of experience in asset-based lending, commercial finance, and structured capital—having closed $250M+ in transactions—Corey previously served as a top business development executive under NYC Mayor Bloomberg, partnering with Fortune 500 corporations including Google, Time Warner, Whole Foods, and Mandarin Oriental on economic development initiatives.

Connect with Corey on LinkedIn: [LinkedIn URL]

I've watched this pattern play out dozens of times: a business owner gets denied for financing, assumes they're not bankable, and shelves their expansion plans.

Here's what kills me — the SBA just rolled out the most significant changes to their lending programs in over a decade, and I'd bet your banker hasn't explained what any of it means for your operation.

The difference between operators who capitalize on regulatory shifts and those who miss them? Understanding what changed well enough to structure your approach around the new reality instead of old assumptions.

Let me break down the five major changes without the policy jargon:

SBA 7(a) loan limit increased to $5.5 million (up from $5 million). SBA Express loans jumped to $500,000 (from $350,000). That's a 43% increase in Express capacity.

Collateral requirements eliminated for loans under $500,000. This is massive. If you're borrowing $400K, the SBA no longer requires lenders to chase down every asset you own. They'll still take what's available, but they can't decline you solely because you lack sufficient collateral.

New equity injection rules for startups and acquisitions. SBA now accepts 10% down for certain business acquisitions (versus 15-20% previously). They also clarified that seller financing can count toward your equity injection in specific deal structures — something that was murky before.

Expanded eligibility for businesses with passive ownership. The previous restrictions on businesses with investors who aren't actively involved got loosened significantly. If you've got silent partners or minority investors, you're no longer automatically disqualified.

Streamlined application process with reduced documentation. The SBA cut their standard documentation requirements by roughly 30% for loans under $350,000. We're talking fewer tax returns, simplified financial statements, faster processing.

If you explored SBA financing before mid-2024 and got declined, the rules changed — revisit it

Loans under $500K no longer require full collateral coverage

Business acquisitions now require less cash down (10% vs 15-20%)

Documentation requirements dropped 30% for loans under $350K

When SBA updates guidelines, banks respond mechanically. They modify workflows, update documentation, send loan officers to compliance training.

But the fundamental way they evaluate your business? That doesn't shift.

I learned this watching deals at every level. The bank's incentive is processing efficiency, not helping you understand what became newly possible. They wait for you to come to them with a request, run it through their updated system, and give you yes or no.

Most operators approach their bank with a need: "I need $750K for this expansion." The bank plugs your numbers into their system — now updated with new SBA parameters — and either approves or declines you.

What you're missing: the way you frame the request, the timing of when you ask, the specific structure you're requesting, which loan program you apply under — all of that determines whether you fit the box. And all of that just changed.

Banks process applications — you need to architect requests

How you frame your request matters as much as your financials

The same business can get approved or declined based on which program you apply under

Your banker won't proactively tell you what became newly possible

Mistake #1: Waiting until you desperately need the capital.

I get it — you're busy running your business. But the best time to secure financing is when you don't urgently need it. These new SBA provisions create opportunities to establish credit facilities before the time-sensitive opportunity shows up.

Most operators do the opposite. They wait until they've got a deal that needs to close in 60 days, then rush into financing conversations with limited leverage and no time to structure properly.

Mistake #2: Asking the wrong lender for the right loan.

Not every bank is set up to maximize what these new SBA changes make possible. Some banks love SBA lending and have streamlined processes. Others treat it like a compliance headache and push you toward conventional products that don't fit your situation.

I've watched business owners get declined by Bank A for something Bank B would have approved in three weeks, simply because of how each institution thinks about SBA programs.

Mistake #3: Optimizing for interest rate instead of deal structure.

An operator gets quoted 8.5% from one lender and 7.75% from another, so they chase the lower rate without asking what they're actually getting.

Lower rate, but requires full collateral coverage? Lower rate, but has a balloon payment in five years? Lower rate, but restricts how you can use the proceeds?

The rate is one variable. Structure is everything.

Apply for SBA financing before you urgently need it — better terms, more leverage

Not all banks are equally good at SBA lending — shop the lender, not just the rate

Deal structure (term length, collateral, covenants) matters more than interest rate

A declined application at one bank doesn't mean you're not bankable

I'll never forget a conversation with a business owner who'd been operating for thirty years. He was refinancing equipment debt, and I was confused why he was paying a slightly higher rate than he could have gotten elsewhere.

He said: "I'm not buying money. I'm buying optionality and timing."

That reframed everything.

Capital is a tool, not a scoreboard. Every significant business I've worked with uses capital strategically. The SBA changes we're discussing expanded the toolkit. If you're treating all debt as equally undesirable, you're operating with one hand tied behind your back.

Timing beats cost in most real scenarios. You know what's more expensive than 9% money? Missing the window on an acquisition that would have doubled your business. Losing a key employee because you couldn't finance the expansion that would have kept them engaged.

Risk transfer vs. risk avoidance. The smartest operators I know don't avoid risk — they structure it. These new SBA provisions let you transfer certain business risks to capital structures that can absorb them better than your operating cash flow can.

Smart operators use debt strategically to accelerate opportunities

Missing a time-sensitive opportunity costs more than "expensive" capital

Proper financing preserves working capital for unexpected challenges

The question isn't "Can I afford this?" — it's "What does this capital let me accomplish?"

I'm not going to pitch you. Here's what I'd do if I were running a business in the $500K-$20M revenue range right now:

Evaluate your current capital structure with fresh eyes. If these SBA changes had been in place two years ago, would you have structured things differently? If yes, you've got optimization opportunities sitting in front of you.

Question what your banker told you 12-18 months ago. If you had financing conversations in 2023 or early 2024 that ended in "no," revisit them. Your banker isn't going to call you to say "Hey, remember when we couldn't do that deal? We might be able to now."

Understand what the new collateral thresholds mean for your situation. If you're looking at loans under $500K, the collateral requirements shifted in ways that benefit operators with strong cash flow but limited hard assets. Service businesses, professional firms, operators without real estate — this changes your options.

Pull your balance sheet and reassess with 2026 rules in mind

If you were declined in 2023-2024, the circumstances may have changed

Loans under $500K no longer require full collateral — huge for service businesses

Don't wait for your banker to explain what became newly possible

Every business owner wants to optimize their cost of capital. Lower rates, better terms, less restrictive covenants. That makes sense.

But the most expensive capital isn't the stuff with high interest rates. It's the capital you should have accessed but didn't — because you were waiting for perfect conditions, or because nobody explained what became newly possible.

These SBA changes won't trend on social media. Your banker might mention them in passing, or not at all.

But for operators who understand what shifted, these changes represent the difference between executing on opportunities and watching them pass by.

At what point does "avoiding debt" become the most expensive decision your business makes in 2026?

How do I know if my business qualifies under the new SBA guidelines?

Start with basics: for-profit U.S. business, under 500 employees or under specific revenue thresholds for your industry. The 2026 changes expanded eligibility for recent ownership transfers, businesses with passive investors, and companies with limited collateral. Get your financials reviewed by someone who works with SBA programs regularly.

What's the difference between SBA 7(a) and SBA Express now that limits changed?

SBA 7(a) goes up to $5.5M, full underwriting, 60-90 day process. SBA Express caps at $500K, streamlined approval, 30-45 day process. Express trades lower maximums for speed. With the new $500K Express limit, more deals can use the faster track.

Does "no collateral requirement under $500K" mean I don't need any assets?

No. It means the lender can't decline you solely because you lack sufficient collateral. They'll still take a lien on available business assets. But if you've got strong cash flow and limited hard assets, you're no longer automatically disqualified.

Should I refinance existing debt to take advantage of these changes?

Depends on your current structure and what you're trying to accomplish. If you're on a balloon payment, have restrictive covenants, or pledged personal assets that the new rules wouldn't require — worth exploring. Run the numbers on prepayment penalties versus long-term benefit.

By Corey Rockafeler

Your CNC machines are paid off. Your forklifts? Owned outright. Your balance sheet shows $1.2M in equipment.

Your bank account shows $47,000.

A competitor just called. They're selling for $850K. You have 30 days to decide. This is the acquisition that doubles your revenue overnight—the one you've been waiting for.

But you don't have $850K. And by the time your bank finishes their 90-day underwriting process, someone else will own your competitor. Private equity wants 25% of your company. The SBA wants your firstborn and three years of tax returns.

The opportunity dies. Again.

Here's what kills me: You actually had the money the whole time. Those paid-off machines? They're worth $1.2M on the open market. You could've accessed $900K in under two weeks. Bought the competitor. Kept 100% ownership. And you'd be running a $15M business right now instead of watching someone else do it.

In this article, you'll discover how to turn owned equipment into working capital in 7-14 days—without bank approvals, without giving up equity, and without disrupting operations. You'll see real examples of $5M-$20M businesses that did exactly this. And you'll learn whether your equipment qualifies and what you can actually access.

Because the next time opportunity knocks, you won't be the one saying "I wish I had known this six months ago."

💡 Key Takeaway:

Owned equipment is working capital you can access in days, not months

Most business owners miss opportunities because they don't know this option exists

This article shows you exactly how it works and whether it's right for your business

Think of it like a cash-out refinance on your house—except it's for your business equipment, and you close in two to three weeks instead of two months.

Here's the simple version: You sell your equipment to a lender. They immediately lease it back to you. You get a check for 70-90% of the equipment’s auction or forced liquidation value. They get an asset-backed investment. You keep using everything exactly as you do right now.

Nothing moves. Nothing changes operationally. Your crew doesn't even know it happened.

The process in five steps:

Equipment appraisal establishes current liquidation value (not market value)

Lender purchases your equipment for a lump sum

You receive cash wire-transferred to your account

Lease agreement is created (typically 3-7 years)

Monthly lease payments begin (100% tax deductible)

Buyback option at end of term (often $1 or fair market value)

Your $1.2M in fully depreciated equipment that shows $0 on your balance sheet? It just became $900K in your bank account. Your CNC machines are still running. Your forklifts are still moving inventory. Your trucks are still making deliveries.

The only thing that changed is you now have capital to actually grow your business.

💡 Key Takeaway:

Sale-leaseback converts equipment equity into immediate working capital

Zero operational disruption—you keep using everything exactly as before

It's a financial transaction, not an equipment transaction

Let me show you what you're up against with traditional options—and why equipment sale-leaseback is different.

See the difference? Let me break down why this matters for your business.

Speed kills—or saves—deals. Banks take months because they're underwriting YOU. Sale-leaseback takes weeks because they're underwriting the EQUIPMENT. Asset-backed means lower risk, which means faster decisions. When that competitor calls about selling, you have two weeks to respond, not two quarters.

Use the money however you want. Banks restrict use of funds. "Working capital only." "No acquisitions." Sale-leaseback? Zero restrictions. Buy a competitor. Stock inventory. Hire ten people. Fund payroll through a slow season. It's your money. You're not borrowing—you're liquidating an asset you continue to use.

Your balance sheet actually improves. The cash influx strengthens working capital ratios. This can actually increase your borrowing capacity elsewhere. Banks see better liquidity. You've freed up collateral for other financing needs.

Keep 100% of your business. No equity dilution. No new partners asking questions. No board seats given away. You built this business—you keep it.

I've closed $250M+ in asset-based financing over 20+ years. I've seen the same pattern dozens of times: Business gets turned down by two, three banks. We appraise their equipment, advance $800K, close in 15 days. The equipment was always there. They just didn't know it was a credit line they were already approved for.

💡 Key Takeaway:

Sale-leaseback is 5-10x faster than bank financing

No restrictions on how you use the capital—it's truly yours

You preserve equity and improve your balance sheet simultaneously

Not all equipment works for sale-leaseback. Here's what does—and what doesn't.

Basic requirements:

Owned outright (fully paid off, no liens)

Good working condition

Clear resale market exists

Minimum $250K+ total value (though we've done smaller deals)

Equipment categories that work well:

Manufacturing: CNC machines, fabrication equipment, metal presses, injection molding equipment, industrial ovens

Transportation: Semi-trucks, trailers, box trucks, delivery vans, fleet vehicles (3+ units work best)

Construction: Excavators, bulldozers, loaders, cranes, backhoes, concrete equipment

Warehouse & Distribution: Forklifts, reach trucks, pallet jacks, conveyor systems, high-value racking

Food Service: Commercial kitchen equipment, walk-in refrigeration, HVAC systems

Medical/Dental: Imaging equipment (MRI, CT scanners, X-ray), dental chairs and equipment

Already pledged as collateral on another loan. Highly specialized equipment with no resale market (custom-built for your specific operation). Poor condition or obsolete technology. Equipment worth under $100K individually (unless part of a larger package).

Here's what trips up most business owners: Your accountant looks at your balance sheet and sees equipment with $0 book value. Fully depreciated. "No value," they say.

Wrong.

Book value is an accounting fiction for tax purposes. Market value is what someone will actually pay for it. I've seen equipment with $0 book value appraise for $1.2M. Your 2019 CNC machine didn't lose its value just because you depreciated it on your taxes.

Book value and market value live in completely different worlds.

💡 Key Takeaway:

Most standard business equipment qualifies if it's paid off and in good condition

Fully depreciated equipment (showing $0 on books) often has substantial market value

Equipment needs a resale market—generic is better than highly specialized

Let me show you exactly what this looks like with three real businesses I've worked with. Numbers, timelines, outcomes—the whole story.

First, understand advance rates: You'll typically get 70-90% of your equipment's auction or forced liquidation value. What determines the rate? Equipment type, condition, age, how easy it is to resell, and your company's creditworthiness.

Now let's look at real deals.

Case Study 1: $5M Precision Manufacturer

The situation: Family-owned machine shop. Been in business 18 years. A competitor called—going out of business, willing to sell for $850K. It was the perfect fit: same customer base, complementary capabilities, trained employees who knew the work.

Problem? They needed the money in 30 days. Their bank said no—debt-to-equity ratios were "too high." Translation: "Come back when you don't need the money."

The equipment: Six CNC machines (5-axis, purchased 2016-2019), metal fabrication equipment, quality control systems. Book value on the balance sheet? $0. Fully depreciated.

Appraised liquidation value? $1.2M.

The deal:

Advance: $900K (75% of liquidation value)

60-month lease term

Monthly payment: $18,500

Time to close: 11 days

What happened: They bought the competitor. Added 15 employees who already knew the customers. Revenue went from $5M to $15M in 18 months. The monthly lease payment? Covered easily by the new revenue.

The owner told me later: "We were so focused on what the bank would or wouldn't do, we forgot we were sitting on the solution."

ROI on that $850K investment? Their business is now worth 5x what it was.

Case Study 2: $12M Regional Distributor

The situation: Growing distributor needed a second warehouse. The location was perfect—30 miles from the main facility, right off the interstate. They needed $600K for buildout, initial inventory, and staffing.

Banks wanted to lend, but the covenants were ridiculous. Inventory turn ratios, debt coverage requirements that would've handcuffed growth. And the owner wasn't interested in giving up equity after bootstrapping for 14 years.

The equipment: Twelve forklifts (various capacities), eight delivery trucks (3-5 years old), high-value warehouse racking system. Total appraised liquidation value: $800K.

The deal:

Advance: $600K (75%)

60-month lease

Monthly payment: $12,400

Closed in 10 days

What happened: Second location opened on schedule. No equity dilution. They preserved their existing credit lines for other opportunities. The new location hit profitability in month nine.

The CFO said something I'll never forget: "We forgot our balance sheet was sitting on $600K we could access in two weeks. We were so obsessed with the P&L."

Case Study 3: $8M Commercial Contractor

The situation: This contractor had a serious problem—and a serious opportunity. Major project pipeline worth $12M, but their bonding company said no. Why? Working capital ratios weren't strong enough. They needed $1.2M to improve the numbers.

Banks were nervous about seasonal cash flow. Construction has feast-or-famine months, and underwriters hate that.

The equipment: Heavy equipment—excavators, loaders, bulldozers, plus a fleet of trucks and trailers. All well-maintained, current models. Liquidation value at $1.6M.

The deal:

Advance: $1.28M (80%—high-quality, liquid equipment commands better rates)

72-month lease term

Monthly payment: $21,100

Closed in 12 days

What happened: Working capital ratios improved immediately. Bonding capacity increased 40%. They won $12M in new contracts they couldn't have bid on before.

Bonus: The lease payments are 100% tax deductible. Annual tax savings? About $55K compared to the old depreciation schedule.

Equipment is still running on job sites every day. Nothing changed operationally.

💡 Key Takeaway:

Real businesses are accessing $600K-$1.2M+ in under two weeks using equipment they already own

Monthly payments are manageable and covered by the growth the capital enables

The pattern is consistent: banks say no, equipment says yes, business grows

Beyond the immediate cash, there are some real advantages here that most business owners miss.

Tax deductions that actually matter:

Your lease payments? 100% tax deductible as an operating expense. Compare that to depreciation, which stretches over 5-7 years and gives you a fraction of the benefit each year.

Example: $15,000 monthly lease payment = $180,000 annual deduction. At a 30% effective tax rate, that's $54,000 in tax savings. Every year.

Under the old depreciation schedule? You might've been deducting $30,000 in year one. The difference—$24,000 annually—is real money.

Your balance sheet improves:

The cash influx immediately strengthens your working capital ratios. Banks notice. This can actually increase your borrowing capacity for other needs—because now you look more liquid, more stable.

You've also freed up collateral. That equipment was just sitting there on your books. Now it's working capital, and your balance sheet looks stronger than it did yesterday.

Cash flow becomes predictable:

Fixed monthly payments. No surprises. No balloon payments lurking three years out. You can budget with confidence.

And here's the strategic piece: You're preserving your credit lines for other opportunities. That bank line? Save it for emergency working capital or a deal that comes up in six months. Your equipment is funding today's growth.

You're matching equipment cost to revenue generation. The machines generate revenue. The lease payment comes from that revenue. It's a natural fit.

Important disclaimer: Tax implications vary depending on your business structure, how the lease is classified, and about a dozen other factors. Always—and I mean always—consult your CPA before making any financing decisions. This is general information, not tax advice for your specific situation.

But here's what I know after 20 years: Most business owners are shocked when their accountant runs the numbers and shows them the actual tax benefit.

💡 Key Takeaway:

Lease payments are fully deductible, creating immediate tax benefits vs. slow depreciation

Sale-leaseback often improves balance sheet ratios and borrowing capacity

Predictable payments and preserved credit lines give you strategic flexibility

Let me be straight with you: Sale-leaseback isn't right for everyone. Here's how to know if it fits your situation.

✅ This is a great fit if:

You need capital fast: There's an acquisition opportunity and the seller wants an answer in 30 days. You landed a huge contract that requires immediate inventory buildup. A piece of real estate came available that's perfect for expansion. Emergency working capital to cover a gap. Whatever it is—you can't wait 60-90 days for a bank.

You want to preserve equity: You bootstrapped this business. You're not interested in investors asking questions at every turn. Or maybe your company's current valuation is too low—you know you're worth more in two years, so why sell a piece now? You want to maintain full control. Period.

Traditional financing already said no: Two banks declined you. Maybe your debt ratios don't fit their boxes. Maybe you had a tough year that spooked underwriters. But your cash flow is actually strong and your business is solid. You just don't fit the template.

Your cash flow can handle it: You're doing $1M-$20M in revenue. The business is growing or stable. You can comfortably handle a monthly lease payment. You've run the numbers—the payment fits in your cash flow without creating stress.

You have valuable equipment: You own $250K+ in equipment. It's well-maintained, good condition. There's a clear resale market—standard manufacturing equipment, trucks, construction machinery, not some custom contraption you built in your garage.

❌ This is NOT a fit if:

Cash flow is shaky: You can't support the monthly payments. Revenue is declining and you're not sure why. You have long seasonal dry periods without cash reserves to cover the gap. Adding a fixed monthly obligation would create stress, not solve problems.

Equipment issues: Your equipment is already pledged as collateral on another loan. It's obsolete—technology moved on and nobody wants to buy 15-year-old machinery. It's highly specialized for your unique operation with zero resale market. It needs major repairs. Or frankly, the total value is under $100K and it's just not worth the effort.

Timing is wrong: You don't actually need the capital—you just think you might someday. Or you actually do have time—three months to close isn't a problem, so go get a bank loan at a lower rate. Sale-leaseback is for speed and flexibility, not just because it exists.

Look, I turn down deals. If your cash flow can't support payments, I'll tell you this isn't the right tool. If your equipment doesn't qualify, I'll tell you that too. There's no point wasting your time or mine on something that doesn't fit.

But if you checked four or five boxes in that "great fit" section? Let's talk.

💡 Key Takeaway:

Sale-leaseback is ideal for businesses with strong cash flow but tight timelines

Equipment quality and cash flow strength matter more than perfect credit

If it's not right for you, it's not right—and that's okay

Here's exactly what happens, step by step. No mystery, no surprises.

Days 1-3: Equipment Appraisal

We get your equipment appraised. Sometimes it's an independent appraiser who comes on-site. Sometimes it's a desktop valuation based on comparable sales data, equipment age, and condition. Either way, we're establishing current market value—not what your books say, but what the equipment would actually sell for today.

Days 3-5: Credit Review

We look at your financials. Last two years of profit and loss statements, balance sheet. We're analyzing cash flow—can your business comfortably support the monthly lease payments? This isn't a deep-dive credit investigation. We're making sure the deal makes sense for everyone.

Days 5-7: Term Sheet

You get a term sheet. It shows the advance amount (how much cash you'll receive), the lease term length, your monthly payment, and purchase options at the end. Everything in writing, nothing hidden. You review it, ask questions, and decide if it works for you.

Days 7-12: Documentation

If you're moving forward, we handle the paperwork. Sale agreement (you're selling the equipment). Lease agreement (we're leasing it back to you). UCC filings (standard security filings). Your attorney can review everything—in fact, we encourage it.

Days 12-14: Funding

Final signatures. Wire transfer hits your account. Done.

Zero operational disruption:

Your equipment never moves. It stays exactly where it is. You maintain possession and use. Your team keeps working. Your production schedule doesn't skip a beat. The only thing that changes is you now have capital in your bank account.

From the day you call me to the day cash hits your account: 7-14 days, depending on how quickly we can move through appraisals and documentation.

Compare that to 90 days at a bank—where you're still not guaranteed approval.

💡 Key Takeaway:

The entire process takes 7-14 days from inquiry to funding

Documentation is straightforward—sale agreement and lease agreement

Zero disruption to operations—equipment stays put and keeps working

Let me address the questions I hear on every single call.

"This sounds like distressed financing. Isn't this what failing companies do?"

No. Fortune 500 companies use sale-leasebacks strategically all the time. It's capital allocation, not desperation. You're choosing speed and flexibility over traditional debt. There's nothing "distressed" about recognizing your equipment has value and choosing to access it.

The distressed move? Waiting until you're out of options. The smart move? Using every tool available when opportunity knocks.

"What if I can't make the payments?"

Then this isn't the right tool, and I'll tell you that upfront. The underwriting process ensures the payments fit your cash flow. We're not here to set you up to fail—we're here to help you grow. Most leases also have early buyout options if your situation changes and you want to own the equipment outright again.

If your cash flow is uncertain, we'll have that conversation honestly. No point moving forward with something that creates stress instead of solving problems.

"Will this hurt my credit or borrowing capacity?"

Actually, it often helps. The cash influx improves your working capital ratios. Banks see better liquidity. This can increase your borrowing capacity elsewhere because you look more stable. And you've freed up collateral—that equipment was just sitting on your books. Now it's working capital, and you can use other assets for different financing needs.

"What happens when the lease term ends?"

You typically have three options: buy the equipment back (often for $1 or fair market value), extend the lease, or return the equipment. The buyout terms are negotiated upfront—no surprises five years from now. Most businesses choose to buy back and own everything outright again. You're basically getting back to where you started, except you had access to $800K for five years that helped you grow.

"Isn't this expensive compared to a bank loan?"

Compare total cost to opportunity cost. What's the cost of NOT having the capital? Missing an acquisition that would've doubled your revenue? Losing a contract because you couldn't stock inventory? Watching a competitor grab the real estate you wanted?

Plus, tax benefits offset the cost. Lease payments are fully deductible. And if the capital helps you grow—which it should—the ROI far exceeds the financing cost.

I worked with a manufacturer who paid $18,500/month for five years. Total cost? About $150K more than a bank loan would've been. But that $900K let them acquire a competitor and triple their revenue. They made the $150K back in the first quarter.

💡 Key Takeaway:

Sale-leaseback is strategic, not distressed—major companies use it regularly

Underwriting ensures payments fit your cash flow before you commit

When used for growth, the ROI typically far exceeds the financing cost

Here's what I want you to remember: Your owned equipment isn't just keeping operations running. It's a strategic financial asset most business owners completely overlook.

While your competitors wait 90 days for bank approvals—or give away 20% of their company to investors—you can access $250K-$2M in 7-14 days. Keep 100% ownership. Keep running your business exactly as you do today.

The businesses that win aren't always the ones with the best products or the hardest workers. They're the ones who recognize their balance sheet is more powerful than they realized. And they move fast when opportunity shows up.

Next time a competitor calls about selling. Next time you need to stock inventory for the busy season. Next time the perfect location becomes available. You'll know exactly what to do.

You won't be the one saying "I wish I'd known about this six months ago."

How much can I access against my equipment?

Typically 70-90% of appraised market value. The exact amount depends on equipment type, condition, age, and how easy it is to resell. We've done deals ranging from $250K to $5M+. A $1.2M equipment portfolio usually generates $900K-$1M in available capital.

How long does the process take?

7-14 days from your first call to cash in your account. Compare that to 60-90 days for traditional bank financing—where you're still not guaranteed approval.

What if my equipment is fully depreciated on my books?

Book value and market value are completely different. Equipment showing $0 on your balance sheet often has significant market value. Your 2019 CNC machine didn't lose its value just because you depreciated it for taxes. We appraise based on current market value, not what your accountant wrote down.

Do I lose use of my equipment?

No. You continue operating equipment exactly as you do now. The only change is financial—you lease what you used to own. Nothing moves. Nothing changes operationally. Your crew won't even know the difference.

What are typical lease terms?

Usually 36-84 months (3-7 years). Terms depend on equipment type and your preferences. Monthly payments are fixed—no surprises, no balloon payments lurking at the end. You know exactly what you're paying every month.

Can I use the money for anything?

Yes. Unlike bank loans, there are zero restrictions on use of funds. Buy a competitor. Stock inventory. Hire people. Fund payroll through a slow season. Expand to a second location. Whatever your business needs—it's your money.

What if I want to buy the equipment back early?

Most leases include early buyout options that are negotiated upfront. If your situation changes and you want to own the equipment outright again, you typically can. Terms vary, but we structure deals with flexibility in mind.

💡 Final Takeaway:

Your owned equipment is working capital waiting to be accessed

While competitors wait months, you can move in days

The next opportunity won't wait—make sure you're ready

Introduction:

President Donald Trump’s tariffs have sent ripples through the U.S. economy, and small businesses are feeling the brunt of the impact. Small businesses are hit hard by high import duties. These tariffs start at 10% on all imports and can exceed 100% for certain goods from countries like China. Costs are rising. Supply chains are disrupted. Profit margins are shrinking. Small businesses don’t have the same resources as big companies. Because of this, they struggle to adapt quickly. This makes them more vulnerable in a changing trade environment.

But it’s not all doom and gloom. Small businesses can spot challenges and seize opportunities. This way, they can navigate this uncertain landscape more effectively. In this article, you'll learn how tariffs impact small businesses. You’ll discover ways to lessen their impact. The you will find creative methods to turn challenges into chances. Whether you’re a business owner or a stakeholder, this guide will equip you with the tools to adapt and thrive.

I. Understanding Trump’s Tariffs

President Trump's tariffs aim to boost domestic manufacturing. They set a 10% duty on most imports. Some items face higher rates, like Chinese steel and aluminum, which hit 145%. These increases target specific industries and rivals. The Tax Foundation says these taxes are among the toughest trade policies we've seen recently. They impact on more than $350 billion in yearly imports.

For small businesses, tariffs pose two main problems: higher input costs and unstable supply chains. Small businesses differ from multinational corporations. They lack diverse suppliers and lobbying power for exemptions. Instead, they depend on stable prices and easy access to global markets. For example, the National Federation of Independent Business (NFIB) reports that 25% of small businesses depend on imported materials, making them disproportionately vulnerable to sudden cost hikes.

The immediate effects are stark. A survey by the U.S. Chamber of Commerce in 2023 found that 40% of small businesses experienced shrinking profit margins due to tariffs. As a result, many had to cut jobs or postpone their expansion plans. These policies also aim to encourage reshoring. This could lead to a long-term shift toward making products at home. The goal is to boost U.S. manufacturing. But small businesses are struggling to keep up with the fast-changing trade scene

II. Challenges Faced by Small Businesses

A. Rising Costs

The most immediate and pervasive challenge is the surge in costs for imported goods. Tariffs on materials like steel, aluminum, and electronics have hit small businesses hard. They must either absorb the extra costs or pass them on to consumers. The National Retail Federation says that “tariffs act as hidden taxes on American families and businesses.” Small businesses take the biggest hit.

⦁ Example: Deer Stags, a New Jersey-based footwear company, faces a 110% tariff on non-leather shoes imported from China. CEO Marc Schneider states, “We’re paying more in tariffs than the actual cost of the shoes. This model is unsustainable for small businesses.”