INTRODUCTION

You’re sitting on a gold mine, but you’re starving to death. It sounds absurd, doesn't it? Yet, after two decades in the trenches of asset-based financing, I see it every single day: the "Equity Hoarder" syndrome. You’ve worked for years to build up millions in commercial real estate value.

But you treat that equity like a religious relic—something to be guarded, protected, and never touched. Here’s the rub: while you’re "protecting" that equity, your business is gasping for air, missing out on inventory buys, or losing talent to competitors because you’re "cash poor" but "asset rich."

This article is your wake-up call. I am going to show you how to stop being a hoarder and start being an architect. We are going to dismantle the myth that debt is always a burden and reveal how a forensic approach to second mortgages can transform your stagnant building into a high-octane liquidity engine.

By the time you finish this, you won’t just see four walls and a roof. You’ll see a strategic ATM that doesn't require a bank's permission to open. As a successful business owners , its time to stop playing defense and start using your balance sheet as a weapon.

I.The Psychological Trap of "Safety"

Equity is a psychological security blanket that often smothers growth. Most small business owners—the ones running the $500K to $20M engines of this country—have been conditioned to believe that a "free and clear" building is the ultimate sign of success. It’s not. It’s a sign of underutilized leverage. In the 2026 market, where capital velocity is the only thing that separates the survivors from the statistics, letting $1M in equity sit idle is a forensic failure.

I’ve witnessed firsthand how owners treat their property like a trophy while their payroll account hits zero. It’s a stagnant philosophy. Look, "safety" doesn't pay the bills when a surprise tax lien hits or a massive expansion opportunity knocks.

Real safety comes from liquidity, not from a deed sitting in a safe.

The Stagnant ATM: Shifting Your Perspective

Stop looking at your real estate as a "building." Start viewing it as a vault of trapped capital that is currently charging you an opportunity cost every single day it remains locked. In my 20+ years of closing over $250M in deals, the most successful entrepreneurs I’ve championed are the ones who understand that real estate is a tool for business expansion, not just a place to park the trucks.

Think of your equity as a stagnant ATM. The money is there, the balance is high, but you’ve forgotten the PIN. My job as an ABL insider is to give you that code. When you shift your mindset from "ownership" to "utilization," the entire architecture of your business changes. You stop begging for terms from suppliers because you have the cash to dictate the terms yourself.

Identifying the Enemy: The Bank and the MCA

To carve this new path, we have to identify the two monsters currently blocking your exit. First, you have the traditional commercial bank. They are the "Slow Death." They’ll ask for three years of tax returns, a blood sample, and your first-born child, only to tell you ninety days later that your "debt-to-income" ratio is 1% off their arbitrary limit. They don't move at the speed of business; they move at the speed of bureaucracy.

Then, you have the "Fast Poison"—the Merchant Cash Advance (MCA). When the bank says no, many desperate owners turn to these predatory daily-debit lenders. They’ll give you the money in 24 hours, sure, but they’ll also take 30% of your daily credit card receipts until you’re bankrupt. It is a debt spiral that is almost impossible to escape.

The Third Path: The Strategic Junior Lien

But wait. There is a third way. We are carving a path that bypasses the bank’s red tape and avoids the MCA’s suicide pact. This is the world of Strategic Junior Liens.

A junior lien—or a second mortgage—is the forensic scalpel of modern finance. It allows you to keep that beautiful, low-interest first mortgage exactly where it is. Why would you refinance a 4% loan into a 9% loan just to get some cash? With a damn war in Iran going on! You wouldn't.

That’s financial malpractice. Instead, we layer a second piece of capital on top. It’s fast, it’s asset-focused, and it’s designed for the "unbankable" hero who has the equity but doesn't fit the "perfect" borrower box.

This is Corey Rockafeler’s Executive Capital Codex in action. We aren't just looking for a loan; we are engineering a liquidity event. We are looking for the hidden mechanics that allow a $5M manufacturing firm to grab $500K in fourteen days to buy out a competitor. That is how you win.

II. Anatomy of a Forensic Second: High-Leverage Liquidity

Cash is oxygen. Without it, your $10M enterprise is just a very expensive hobby. Most owners I champion are "Asset Rich and Cash Poor," a state of existence that is as dangerous as it is common.

You have millions locked in brick and mortar, yet you’re sweating the Tuesday payroll because your receivables are lagging. That’s a structural failure.

A forensic second mortgage fixes the plumbing.

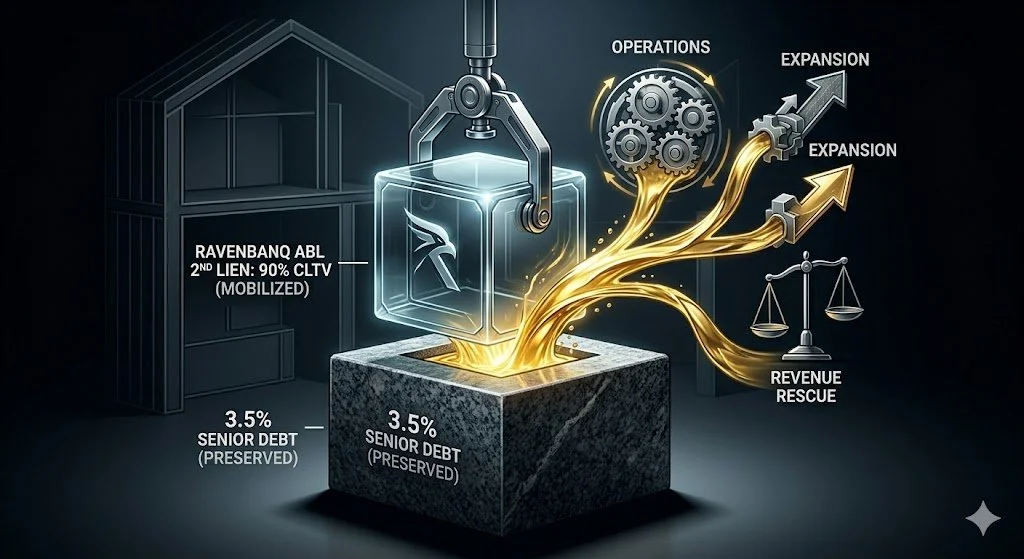

We don't touch your first mortgage. Why would you? If you’re sitting on a 3.5% rate from three years ago, refinancing the whole stack into today's 8% or 9% market is financial suicide. Instead, we "wrap" the equity through the Ravenbanq ABL 2nd Mortgage Solutions. We leave the primary debt alone and layer a junior lien on top to bridge the gap.

It’s about the Combined Loan to Value (CLTV).

If your building is worth $2M and you owe $800k, you have $1.2M in "dead" equity. Most banks will stop at 50% or 60% total leverage. They’re timid. We push the ceiling. With the right forensic structuring, we can hit 75%, 80%, or even 90% CLTV, depending on the asset's story and the speed you need to move.

III. The Ravenbanq Sprint: Bridging the "Unbankable" Gap

Speed kills the competition. In the world of $500k to $20M businesses, the best deals don't wait for a bank's sixty-day underwriting cycle. They go to the person with cash in hand. Our primary bridge solution within the Ravenbanq portfolio acts as a "story" lender.

We aren't obsessed with your FICO score.

I’ve witnessed this program fund deals for owners with recent bankruptcies or messy tax liens, provided the real estate has meat on the bone. We look at the exit strategy. How are you going to pay this back? If the logic holds, the money flows.

Our secret weapon is Cross-Collateralization.

Suppose your real estate equity is a bit thin for the amount you need. We don't just walk away like a traditional lender. We will "cross" the loan against your heavy machinery, your fleet of trucks, or other titled vehicles. We look at your entire balance sheet as a puzzle to be solved, not a list of reasons to say "no."

Look at the speed. I’ve utilized this solution to close $500k seconds in under two weeks. Compare that to your local "community" bank that wants three years of audited financials and a personal guarantee from your grandmother. This is the high-octane fuel for the "unbankable" hero who needs to execute now.

IV. The Institutional Pillar: Stand-Alone Power & Mixed-Use Mastery

Stability matters. While the bridge is the sprint, our long-term Ravenbanq 2nd mortgage is the distance engine. We offer something almost unheard of in the commercial space: a 30-year fixed-rate second mortgage that behaves like a residential loan but plays in the commercial league.

It’s a "Non-QM" masterpiece.

We don't care about your tax returns. If you’ve worked with a clever CPA to maximize your write-offs—which most of my clients have—your tax returns probably show you making twelve dollars a year. A bank sees a loser. I see a smart business owner. We qualify you based on 12 or 24 months of bank statements or a simple P&L.

Then, there is the 90% CLTV Stand-Alone 2nd. This is for Primary, 2nd Home, & Investment homes.

This is the peak of leverage. You can keep your first mortgage at $1M, and if the property is worth $2.5M, our Ravenbanq solution can drop a second mortgage of over $1M on top of it. That is pure, raw liquidity. It’s the difference between wondering if you can afford that new production line and actually ordering it.

Don't overlook the Mixed-Use play.

If you own a building with 2 to 8 units—maybe your office is on the ground floor and there are apartments above—we use a DSCR (Debt Service Coverage Ratio) model. We look at the rent. Does the property pay for itself? If the answer is "yes," you’re approved. Your personal debt-to-income ratio is irrelevant. The building is the borrower.

V. Case Study: The "Revenue Rescue" (Forensic Execution)

Math doesn't lie. But it can certainly suffocate you.

I recently walked into a situation with a mid-sized manufacturing firm in New York. The owner was a visionary with a $2.2M commercial facility owned through his holding company. On paper, he was a titan. In reality, he was drowning.

He had $450,000 in Merchant Cash Advance (MCA) debt.

These were "Daily Debit" monsters. Every single morning, before he even turned on the warehouse lights, these lenders pulled $3,500 out of his operating account. It was a suicide pact. He couldn't buy raw materials. He couldn't bridge the gap on his 90-day receivables. He had $1M in equity in his building, but his "paper losses" on his 1040s made him radioactive to his local community bank.

He was "unbankable." Or so he thought.

I performed a forensic audit of his balance sheet under our Ravenbanq ABL 2nd Mortgage Solutions. We didn't touch his first mortgage—a beautiful 3.2% relic he’d locked in during the pandemic. Instead, we layered a stand-alone junior lien at 85% CLTV.

We used a bank-statement qualification model.

We ignored the tax returns. We looked at the cash flowing through his business over the last 12 months. The property qualified itself. We closed the $500,000 second mortgage in seventeen days.

The result? Total transformation.

We wiped the MCA debt off the map. His monthly debt service plummeted from $70,000 (across all daily debits) to a manageable $6,200 monthly payment. We didn't just "find money." We manufactured $63,800 in monthly "found" liquidity. That is the power of the Architect over the Hoarder. He didn't need more sales; he needed better structural engineering.

VI. Strategic Deployment: When to Pull the Trigger?

Timing is everything.

You don't take a second mortgage because you're "bored" or want a new car. You take it to solve a specific capital constraint. In my 20+ years, I’ve identified three "Strike Zones" for Ravenbanq solutions.

Strike Zone 1: The Opportunity Gap.

A competitor is going out of business. You can buy their inventory for 30 cents on the dollar, but you need $300k by Friday. A bank will take three months. We take two weeks.

Strike Zone 2: The Toxic Debt Refinance.

You’re trapped in the MCA cycle. You’re paying 40% effective interest. We use your "dead" equity to kill the poison and give your cash flow room to breathe.

Strike Zone 3: The Asset-Based Expansion.

You need to buy a $1M CNC machine. The equipment lender wants 20% down. You don't want to drain your cash reserves. We pull the 20% out of your building equity, keep your cash in the bank, and secure the growth.

It’s about leverage, not just debt.

Many owners worry about "putting the building at risk." Here is the reality: Your building is already at risk if your cash flow is so tight that one bad month could sink the ship. Diversifying your risk by moving equity into liquid working capital is the safest move you can make.

VIII. Closing: Moving the Weight

Stop waiting for the "perfect" economic climate. It doesn't exist.

The 2026 market belongs to the agile. If you’re sitting on seven figures of equity while struggling to fund your next big move, you aren't being "conservative"—you’re being stagnant. The walls of your office shouldn't be a cemetery for your capital. They should be the fuel for your future.

What will your legacy be? The guy who owned a building, or the leader who built an empire?

The choice is a matter of architecture.

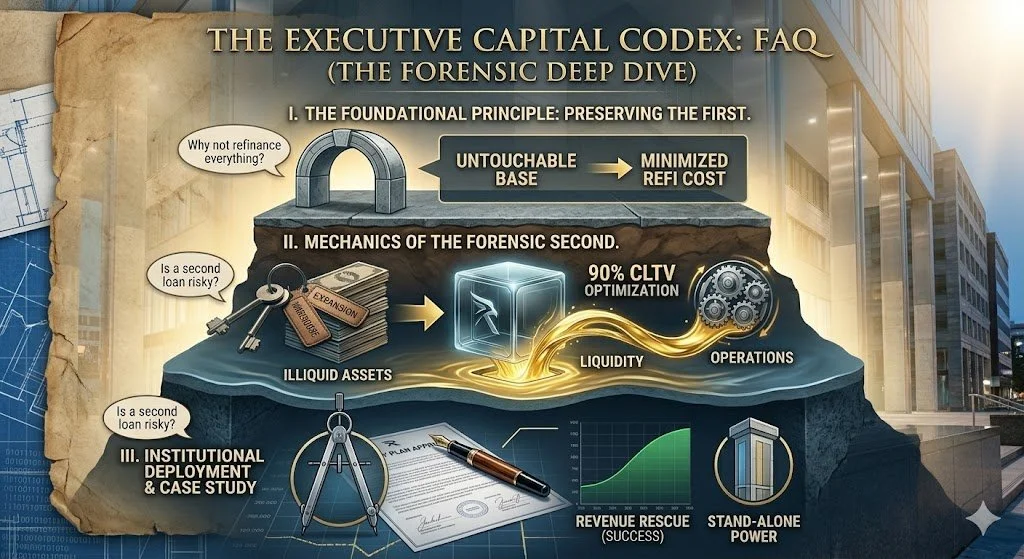

The Executive Capital Codex: FAQ (The Forensic Deep Dive)

You have questions. I have the scars from 20 years of answers.

Q: "Will my first mortgage company find out?"

This is a frequent fear. The reality is that Ravenbanq 2nd mortgage solutions are stand-alone junior liens. They don't require the permission of your first mortgage holder. You aren't "breaking" your first mortgage; you’re just adding a floor to the building.

Q: "My credit is shot. Am I out?"

Hardly. We aren't credit-driven; we are asset-driven. If you have equity and a clear exit strategy—meaning you can show us how the business generates the cash to pay the note—the FICO score is a secondary conversation. I’ve closed $1M deals for guys with 580 scores.

G: "What's the max I can get?"

We push the boundaries. While banks sleep at 65%, our solutions can hit 90% CLTV on the right assets. If your building is worth $2M and you owe $1M, we can often find another $800k.

Q: "Is this only for warehouses?"

No. We look at ALL type of revenue generating properties. They include retail, office, industrial, and mixed-use. If it has four walls and a deed, it’s a candidate for a forensic audit.

About the Author

Founder & Principal Advisor, Ravenbanq

Corey Rockafeler, as the driving force behind Ravenbanq, specializes in Asset-Based Lending (ABL), Fintech, and Real Estate Lending. With a track record of closing $250M+ in financing business, Corey helps business owners secure needed capital through tailored ABL solutions.